Green Bonds' Growing Role in ESG Investing

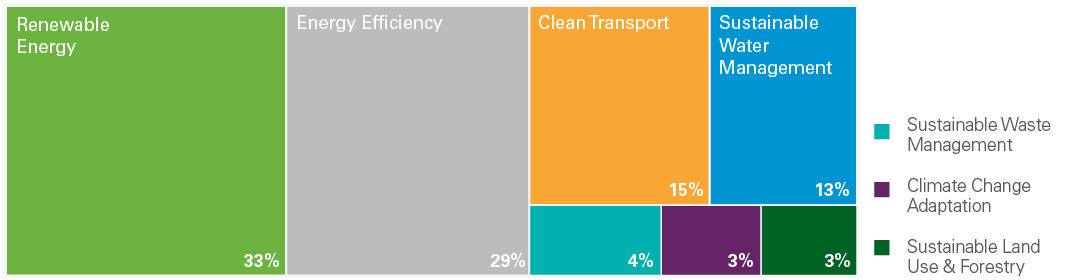

Source: Lazard Asset Management Summary Green bonds are an important component of ESG investing. They align investors with environmentally friendly projects and provide crucial social benefits. Demand for green bonds is surging. Green bond issuance has steadily increased since 2007 and is expected to surpass $250 billion in 2018. As the global economy shifts to a low-carbon footprint, portfolios that have proactively reduced their carbon exposure may be better positioned to outperform the broad market. We believe integrating ESG factors and green bonds into a portfolio may lead to better returns. The focus on responsible investing has grown rapidly over the past decade, and it is now considered mainstream in many parts of the world to incorporate environmental, social, and governance (ESG) factors into investment analysis. Since the Principles for Responsible Investing (PRI) initiative was launched in 2006 with support from the United Nations, more than 1,800 signatories, nearly 400 of which manage roughly $70 trillion of assets, have joined this effort (Exhibit 1). There is also increased awareness of the UN Sustainable Development Goals (SDGs) which cover a broad range of economic and social development issues. Here, we describe green bonds and their underlying principles, and explain the market for these securities as well as their issuance. The Principles for Responsible Investing (PRI) is the world’s leading proponent of responsible investment. Asset owners and investment manager signatories are required to report on their responsible investment activities annually through the PRI Reporting Framework. Source: PRI Why Green Bonds? A green bond is a standard fixed income instrument whose proceeds are used to finance "green” or environmentally friendly projects. This type of investment is compatible with an ESG framework (especially the environmental and social factors). In the past, investors have tended to focus more specifically on governance factors to better understand the risks and opportunities associated with lending to different entities. Today, however, instruments like green bonds are allowing investors to directly address the environmental and social aspects of their investments. Proceeds from green bonds issued to finance solar or wind projects, for instance, may also provide clean water, lessen pollution, and introduce a sustainable energy source to remote areas. From an investment perspective, green bonds provide an ESG-friendly option for investors wanting to navigate the transition away from fossil fuel investments and reduce exposure to "stranded assets,” such as coal companies. Momentum for green bonds has strengthened as various global institutions and organizations increasingly divest their portfolios away from fossil fuel investments as they focus on mitigating or addressing climate change. This trend should help support strong valuations for green bonds. Issuance is also increasing as the "labeled” (bonds that are certified as green) and "unlabeled” (projects that are linked to environmental benefits but are not certified green) markets evolve. We believe that countries and companies that can reduce carbon emissions and adapt to, or mitigate climate change will be better positioned to prosper. Green bonds are particularly important to the clean energy, infrastructure, and transportation industries as they allow countries and companies to obtain funding to achieve positive and sustainable environmental and social goals. Clean Energy Climate change is a potential disruptive factor for asset valuations. In 2015, the United Nations Climate Change Conference (COP 21) convened with the goal of securing global commitments to reduce greenhouse gas emissions in order to limit the increase in global temperatures to 2 degrees Celsius. Today, 195 countries have signed on to this initiative and many cities and companies have adopted their own targets for reduced emissions. We believe the energy revolution will not only provide positive environmental benefits, but will also have a significant effect on the investment landscape. In recent years, investment in wind, solar, and other renewable energy technologies has grown fast, and we expect this momentum to continue (Exhibit 2), particularly in Europe, China, and India. Even in the United States, renewable energy represents over 15% of power generation. Green bonds are a vehicle for financing sustainable infrastructure projects, which are increasing in number. The cost of developing needed global infrastructure by 2025 is estimated to be at least $78 trillion. These projects range from building new transportation facilities and energy efficient buildings to enabling sustainable water management and sustainable agriculture. Green bonds lend themselves well to public-private partnerships where private sector efficiencies are combined with public sector governance. These investment collaborations tend to be relatively more stable as both parties have aligned interests. With global monetary policy largely exhausted in many countries, green bonds could help support infrastructure spending. This could provide much-needed fiscal stimulus for local and global growth, while also helping to achieve environmental and social goals. Electric Vehicles Gasoline-powered vehicles, or internal combustion engine vehicles, account for a meaningful part of global oil consumption. Meanwhile, the growth of the global electric vehicle (EV) market is expected to reduce demand for fossil fuels and a growing number of countries are considering banning the sale of new gasoline-powered vehicles (Exhibit 3). Norway, a large petroleum-producing country, was an early proponent of this trend and currently boasts EV penetration close to 50%, which is in line with its goal to ban new sales of internal combustion engine vehicles by 2025. Green bonds are a great way to participate in "disruptive technologies” within the transportation/EV sector. Proceeds from some of these bonds have been used to support development of car batteries and charging station infrastructure. Toyota and Geely (which manufactures taxis used in London) have both issued green bonds to help finance EV research and manufacturing. Green Bond Issuance and Use of Proceeds Green bond issuance has steadily increased since 2007, when the European Investment Bank issued the first "Climate Awareness Bond.” Total issuance surpassed expectations in 2017 and is expected to exceed $250 billion in 2018 (Exhibit 4). Citigroup estimates that green bonds could grow into a trillion dollar conduit for climate-related investments by 2020 and SEB, a Swedish bank, predicts that 20% of all bond issuance may be "green” within a few years. Banks and corporations in the developed world are expected to issue more green bonds. There should also be active issuance by sovereigns and municipalities and we expect a greater number of green securitized bonds. In the emerging markets, Chinese companies had significant green bond issuance in 2016 and other countries, such as India, Kenya, and Fiji, have started to issue green bonds. While green bond proceeds have been put to use in many ways, in the past they have primarily been channeled to renewable energy and energy efficiency projects (Exhibit 5). Efforts to develop low-carbon transportation and sustainable water and waste management are increasing and green bonds are becoming a more commonplace form of financing for urban metro and rail projects. Export Development Canada (EDC) and Kommuninvest are two organizations that are heavily committed to supporting "green” projects. Financial institutions, such as Barclays, have also issued green bonds. As added incentive, the European Commission is considering lower capital requirements for bank lending to select "environmentally friendly” projects. Green Bond Principles and Governance Rules continue to emerge to govern the nascent green bond sector. The Green Bond Principles (GBP) are currently the most well-established framework for evaluating these instruments. The GBP were developed by the International Capital Markets Association and have four components: use of proceeds, process for project evaluation, management of proceeds, and project reporting. These are voluntary guidelines and the determination of what constitutes a green bond is still left to the issuers and underwriters. Many issuers choose to secure an independent review and to this end a Climate Bond Certification is generally recommended. Examples of organizations who conduct this independent verification include Sustainalytics, Cicero, DNV GL, and accounting firms such as Ernst & Young and Deloitte. Moody’s was one of the early entrants to the green bond "second opinions” market in 2016, and constructed a methodology to assess the environmental credentials of issuers. Its framework evaluates the issuer’s approach to managing, administering, allocating, and reporting on the projects financed by green bonds, and produces a composite grade ranging from "Excellent” (GB1) to "Poor” (GB5). The use of proceeds carries the largest weighting (40%) in their score. S&P also launched a Green Evaluation Tool to score green projects according to the quality of governance, transparency of a transaction, and the environmental impact associated with the project. As investors continue to integrate sustainability into their investment process, we expect that green bond standards and classifications will continue to develop in scope and detail. Green Bond Investment Opportunities The Bloomberg Barclays MSCI Global Green Bond Index draws heavily from the GBP and has a stated aim to offer investors an objective, robust measure of the green bond market. The index’s characteristics have evolved over the past few years, but agency and supranational issuers still dominate, accounting for almost half of all green bond issuance. Sovereign issuers were very active in 2017, and France now has the biggest single green bond outstanding at €9.7 billion. US mortgage lending agency Fannie Mae topped the charts with over $27 billion of green mortgage-backed securities issuance aimed at funding a multifamily green initiative program. Corporations representing industries ranging from financials to utilities to industrials are also increasing their market share. Municipal issuers are participating, but some of these issue sizes are small, and as such they may not be accessible to institutional investors. The index’s currency breakdown is largely euro- and US dollar–denominated, along with roughly 10%–15% represented by Canadian dollars, British pounds and others. This index also excludes high yield securities as well as Chinese renminbi–denominated green bonds. Ultimately, we believe that an active and tactical approach to investing in green bonds may allow investors to better manage risk factors, such as those relating to currencies and rates. In addition, the index only includes "labeled” green bonds, and there may be additional opportunities in bonds not labeled "green” whose proceeds are applied toward advancing positive environmental and social causes. An example of an attractive relative value opportunity can be seen in Mexico’s first green bond issuance, initiated by Nacional Financiera (NAFIN), a development bank, whose proceeds are being used exclusively to fund and invest in wind projects (Exhibit 6). Not only is NAFIN supported by an explicit guarantee from the Mexican government, but the bond was also issued at an attractive spread over Mexican government bonds. The issuer obtained an independent review from Sustainalytics, is Climate Bond Certified, and received the "Green Bond of the Year” award for 2015. Mention of these securities should not be considered a recommendation or solicitation to purchase or sell the securities. It should not be assumed that any investment in these securities was, or will prove to be, profitable, or that the investment decisions we make in the future will be profitable or equal to the investment performance of securities referenced herein. There is no assurance that any securities referenced herein are currently held in the portfolio or that securities sold have not been repurchased. The securities mentioned may not represent the entire portfolio. Source: Lazard, Bloomberg An Important Element of ESG Investing The green bond market is rapidly growing and evolving, but it is still in the early stages of development. A key driver of its momentum is the increasing engagement with ESG factors and sustainable investing on the part of issuers and investors. Green bonds offer governments and companies a way to capitalize on this trend. As society focuses on reducing its carbon footprint, we believe portfolios that recognize this secular trend and proactively reduce their carbon exposure may be better positioned to outperform the broad market. We believe an investment approach that emphasizes sustainability is better placed to add value in the long run. Based on our observations as managers of global fixed income portfolios, the integration of ESG factors and green bonds into the investment process can help investors reap opportunistic gains as well as defend returns.

0 Comments

|