|

Delivering America’s Energy Future

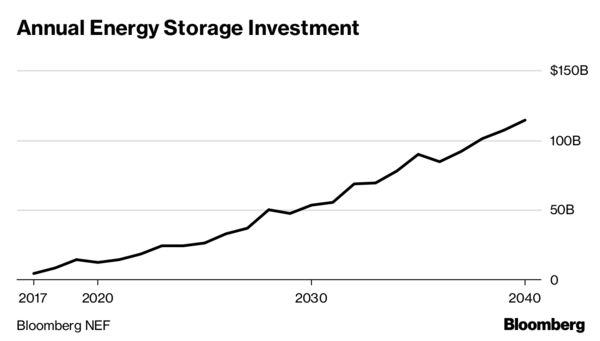

http://www.eei.org/issuesandpolicy/finance/wsb/Documents/EEI_WSB_Remarks.pdf Presentation: http://www.eei.org/issuesandpolicy/finance/wsb/Documents/EEI_WSB_Presentation.pdf Electric companies are evolving practices concerning the environment, social responsibility, and corporate governance. Electric Power Industry Outlook Mahatma Gandhi once said, “The future depends on what we do in the present.” Each day, the member companies of the Edison Electric Institute (EEI)—the nation’s investor-owned electric companies—are hard at work, providing the reliable, affordable, secure, and increasingly clean energy that our customers need and expect. At the same time, EEI’s member companies are tran- sitioning to cleaner energy resources and reducing their carbon emissions; modernizing the energy grid and building smarter energy infrastructure; and delivering innovative energy solutions in a rapidly changing world—all while sustaining financial health in a positive regulatory environment. These are the fundamental principles, the strategic pillars, that continue to guide us. Today, we are pleased to deliver our annual briefing on the state of the electric power industry. As we will outline, we are excited and optimistic about the opportunities we have before us. More important, we are confident the transformation we are leading will deliver America’s energy future. We also are proud that our member companies are woven into the fabric of our nation. As an industry, we support more than 7 million jobs across the country— about 1 out of every 20 jobs. We are responsible for $865 billion of our nation’s GDP—about 5 percent. And, EEI’s members contribute more than $400 million each year to charitable causes, not to mention the many hours of volunteer work done by company employees in their local communities. With the support of our membership, we entered 2019 in a strong position, ready to build on the momentum we have established. We know that our job of developing common industry positions and advocating for them broadly is as vital as ever. We are committed to putting our customers first, to maintaining reliability, and to keeping electricity prices low for all customers, especially low-income customers. We are advocating for policies that focus on outcomes, support progress, and accelerate inno- vation. And, we are working with the Administration and with policymakers on both sides of the aisle in Congress, and in the states, to find common ground and to advance policies that benefit our customers. We can, and we must, work together to achieve meaningful progress with our nation’s energy priorities. We have a tremendous and unparalleled opportunity in front of us to accelerate the reinven- tion of our business, to grow and to thrive amidst all the change. The Clean Energy Transformation It truly is incredible just how dramatically our nation’s energy mix has changed over the past decade. Today, more than one-third of our electricity comes from carbon-free sources (including nuclear energy and hydropower and other renewables), and another one-third comes from natural gas. And, since 2005, the percentage of renewable sources in the energy mix has quadrupled—more than half of new electricity generation capacity each year is wind and solar. By 2024, our industry plans to retire more than 100 gigawatts of coal-based electricity generation. As electric companies continue to transition their gener- ating fleets, their emissions are dropping signifi- cantly. At the end of 2017, the electric power sector’s carbon dioxide (CO2) emissions were 28 percent below a 2005 baseline, the lowest level since 1988 and lower than the transportation sector since 2016. This impressive trend is expected to continue, as many EEI member companies have announced significant voluntary commitments to further reduce CO2 by 2030 and 2050, many of which aim to reduce emissions by 80 percent below 2005 levels by 2050. To ensure that the clean energy transformation reaches its full potential, EEI is advocating for public policies that increase research and development funding and support for the range of technologies needed to achieve clean energy goals, including energy efficiency, energy storage, renewables, existing and next-generation nuclear, other carbon- free technologies, and carbon capture utilization and storage. We are calling on policymakers to help electrify the transportation sector—recognizing that transporta- tion emissions now are the largest source of emis- sions in the United States—by modernizing federal transportation programs to encourage investments in electric transportation and charging infrastructure. Transportation electrification provides an opportu- nity to leverage the significant reductions in power sector emissions to achieve reductions in transpor- tation sector emissions. We also are urging policymakers to support ongoing investments in the energy grid, which are necessary to increase cost-effective electrification and to inte- grate advanced clean energy technologies reliably and affordably. And, we are promoting the develop- ment of more robust battery technologies for both electric vehicles and energy storage. An estimated 280 megawatts (MW) of advanced energy storage were installed in 2017, up 400 percent from 2014, and it is projected that another 338 MW of battery storage capacity were installed in 2018. Energy storage facilitates the integration of renewable energy resources into the energy grid. Today, our customers increasingly are informed about energy, and it matters to them where it comes from and how they use it. Saving money, using less energy, and protecting the environment are all important to them, and to us. With the right poli- cies in place, EEI’s member companies can further reduce their emissions, help dramatically reduce the most significant emissions from other industries, and deliver the clean energy future that Americans want and expect. The Benefits of Electric Transportation One area that touches all three of our strategic pillars and clearly demonstrates how the energy transfor- mation has extraordinary potential for our customers and our businesses is electric transportation. As an industry, we are passionate about electric transportation, and especially electric vehicles. Last year was a watershed year for EVs. In late October, we reached a milestone—more than 1 million EVs on America’s roads—that we celebrated with automakers, infrastructure providers, environmental organizations, and policymakers. Today, the momentum from manu- facturers around the world truly continues to surge. Electric transportation is a huge win for our industry: it grows load; attracts new customers; reduces carbon emissions and improves air quality; and helps reinforce the energy grid. A new report from EEI and the Institute for Electric Innovation projects that we will reach 2 million EVs by early 2021, and more than 18 million by 2030. About 9.6 million charge ports will be required to support them—a significant investment in EV charging infrastructure. EEI’s member companies are taking the lead, investing more than $1 billion over the next five years to deploy charging infrastructure and to create customer programs and projects to accelerate elec- tric transportation. From a policy perspective, we will continue to promote transportation electrification to benefit the environment and to enhance customer options. We will support investments in electric transportation and the necessary charging infrastructure. And, we will continue to support the EV tax credit for new vehicle purchases. Last year, EEI worked with auto manufacturers to file comments on the Administration’s proposed repeal of the corporate average fuel economy (CAFE) stan- dards and the greenhouse gas vehicle standards that highlight the importance of EVs in addressing a range of air quality issues and electric companies’ role in deploying charging infrastructure. EEI is urging the Administration to finalize these standards to include compliance flexibilities focused on EV deployment. We also believe the Administration should work with California to find a solution that would allow the state to address its significant local environmental concerns, while respecting the Clean Air Act’s balance of state and federal authority. Meeting Customers’ Expectations As an industry, our customers are at the heart of everything we do. We know that our customers have high standards along with changing needs and expectations. And, we believe it is more important than ever that we focus on enhancing the customer experience and providing the energy solutions that customers want. Today, EEI’s member companies continue to change the way they provide products and services to customers and to individualize those products and services—for large commercial and industrial customers, as well as residential customers. Last year, under the guidance of EEI Chairman Lynn Good, we launched a new customer-focused initiative designed to improve the customer experi- ence. Through this initiative, EEI is working with our member companies to identify successful and inno- vative approaches to enhance customer operations and customer engagement for residential customers in regulated markets. Among the emerging energy solutions we have identified to date: Companies today are investing in energy management mobile apps to give customers instant access to their energy use data, more control over their energy use, and opportunities to save money on their energy bills. They are creating online energy marketplaces to deliver a branded and curated e-commerce experience to meet customers’ expectations of service and convenience. They are using technology and data to deepen relationships with customers and to help them better engage with their energy use. And, they are making bill payment easier by enabling new payment channel options and reducing fees. For our large customers, we are working to develop an electric industry carbon reporting template to simplify the customers’ process of accessing data for their sustainability reporting. We also are working with large customers to provide sustainable and integrated energy solutions that meet their needs. In addition, EEI is working with large customers on fleet electrification opportunities, including plan- ning and coordination for charging infrastructure to remove barriers and to help create a seamless transition to fleet electrification. And, we continue to work with our member companies on how best to engage with local communities on their smart community goals. We know that it is critical that we continue to deliver more tailored energy solutions that meet the unique needs of our diverse customers. The Political Backdrop The 116th Congress that convened on January 3 is a group of lawmakers unlike any in the past. This is the most ethnically and gender diverse Congress in history and includes a record number of women, as well as our nation’s first Native American Congresswomen. Newcomers now hold seats left open by a wave of retirements and an unusually large number of incum- bents who lost in last November’s midterm elections. The U.S. House of Representatives has 100 first-time members, while the U.S. Senate has 11. For the first time in more than a decade, the economy was not the top issue for voters in November. Exit polling revealed that voters were most concerned about health care, but it was ranked first by a plurality and not a majority. Economic concerns ranked second, while energy issues did not rank among voters’ top concerns. Energy is part of the broader discussion now. Climate change and other environmental issues quickly have emerged as priorities for the House Democratic freshmen. The newly formed Select Committee on the Climate Crisis, chaired by Representative Kathy Castor, will have a broad mission scope regarding climate change. While the select committee will not have authority to subpoena or write legislation, it will be required to provide policy recommendations to the House by March 31, 2020. While we expect to see much discussion in the House around efforts to mitigate and adapt to the effects of climate change, passage of climate pricing legislation is unlikely with Republicans in control of both the Senate and the White House. The two parties could make progress on other climate-related policies, however. Looking at other issues, there is broad congres- sional agreement on the need for an infrastructure package, but not on what one should contain or how to pay for it. Legislation related to energy grid secu- rity also may attract bipartisan support. EEI always has taken a bipartisan approach to issues and has worked across party lines to advance our policy priorities. And, we will do the same with the new Congress. Of course, working with federal lawmakers is only part of the equation. Much of the policy debate and direct oversight of our industry happens in the states. At the state level, numerous governorships and state houses flipped in 2018, having an important impact on environmental and energy policy discussions and legislation, especially regarding renewable portfolio standards and carbon emissions. One of the biggest stories on Election Day was ballot initiatives. We had two enormous ones in our industry: in Nevada on Question 3, a retail choice initiative, and in Arizona on Proposition 127, an aggressive renewable portfolio standard. Both initia- tives would have raised customer electricity prices significantly, and voters overwhelmingly defeated them. As we look ahead to the 2020 elections, the outcomes of numerous ballot initiatives will be crit- ical for energy policy in many states. The Regulatory Landscape Turning to the regulatory arena, we expect some important decisions will be handed down this year. At the federal level, the Environmental Protection Agency likely will finalize its repeal of the Clean Power Plan and issue its replacement rule, the Affordable Clean Energy rule. EEI submitted comments advo- cating that any final rule should consider the ongoing clean energy transition by providing states and sources with significant flexibility when determining compliance measures. Also on the environmental policy front, EEI has long advocated for a replacement of the problematic 2015 Waters of the United States rule. Last year, EPA and the Army Corps of Engineers proposed a replace- ment, an important step in providing EEI’s member companies with greater regulatory certainty and clarity, while avoiding substantial new operating requirements and increased customer costs. Regulatory certainty regarding the continued opera- tion, closure, and clean-up of coal ash basins also is needed. EEI is supporting EPA’s efforts to revisit the coal ash rule by establishing realistic timeframes for the closure of ash basins. EEI supported retention of the Mercury and Air Toxics Standards rule, which the industry implemented and which has led to significant mercury reductions. It appears that EPA will continue with its reconsideration of this rule. This in no way lessens our commitment to a healthy environment and to transition to an even- cleaner generation fleet. At the Federal Energy Regulatory Commission (FERC), it has been a challenging period, marked with significant commissioner turnover and the tragic death earlier this year of Commissioner Kevin McIntyre. Despite this, the Commission has managed to make slow but meaningful progress on a few key policy issues, such as return on equity and pancaked complaints. FERC needs a full comple- ment of commissioners to enable progress on the wider range of issues that have been identified by Chairman Neil Chatterjee. EEI and our member companies have a number of priorities at FERC, with holistic reform of the Public Utility Regulatory Policies Act (PURPA) at the top of the list. PURPA is 40 years old. It is an outdated statute that leads to billions of dollars in excess costs for customers. EEI will continue to advocate that the Commission implement regulations to recognize the greater competition in today’s electricity markets and to better protect customers. Also at FERC, EEI is focused on the value that trans- mission will play in bringing about the connected and clean energy future. Issues such as returns on equity, transmission incentives, and Order 1000 are likely to be on the Commission’s docket, and EEI will advocate for policies that recognize the impor- tant role that transmission will play, including in any discussion on resilience. We believe FERC should continue to address energy price formation issues to ensure that energy prices reflect the cost to operate the system. This will help ensure that resources are compensated for the service they provide to the energy grid. At the state level, EEI will continue to advocate for industry priorities in regulatory forums and proceed- ings to ensure the sustained growth of the industry, including an increased focus on the value of the energy grid and the importance of recovery mecha- nisms based on cost-causation. In particular, EEI and our member companies will advocate for rate and regulatory reforms that recog- nize customer customization and segmentation, while ensuring fairness by balancing economic effi- ciency, equity, revenue adequacy, bill stability, and customer satisfaction. Infrastructure Policy Smarter energy infrastructure is key to giving customers the energy solutions they want. To ensure that we can meet our customers’ needs, EEI member companies invest more than $100 billion each year to make the energy grid smarter, stronger, cleaner, more dynamic, and more secure. Since 2005, EEI member companies have invested more than $445 billion in transmission and distri- bution infrastructure. These investments help to increase the integration of renewable resources, power the rapid increase of electric vehicles, and facilitate the adoption of a broad array of smart tech- nologies to better serve our communities. However, it takes more than investment alone. Critical policy changes are needed. EEI continues to work with the Administration on a variety of important energy infrastructure siting and permitting issues that impact both electric transmis- sion lines and natural gas pipelines. These issues include rights-of-way permits, vegetation manage- ment, avian protection, and reforms to the Clean Water Act, Endangered Species Act, and National Environmental Policy Act. While the Administration continues to advance these initiatives, the timing for action is uncertain. At all levels, energy infrastructure siting and permit- ting processes often are burdensome, restrictive, and duplicative, creating delays that are unnecessarily costly to companies and customers. These processes need to be updated to reflect today’s realities. We also continue to advocate that everyone who uses the energy grid should share equitably in the costs of maintaining it. And, we believe policies should allow electric companies to plan, build, and operate the energy grid as a platform to integrate a diverse set of emerging technologies. Storm & Wildfire Response Last year, Mother Nature tested our industry’s resolve with four nor’easters, devastating wildfires, and a pair of major hurricanes, Florence and Michael, among other events. Using what we have learned from previous storms, EEI implemented comprehensive and aggressive responses to each event. We leveraged the industry-government partnership forged through the CEO-led Electricity Subsector Coordinating Council (ESCC) to facilitate timely communications and to coordinate resource alloca- tion and response efforts. Mutual assistance is a hallmark of our industry—our companies have some of the most talented, caring, and dedicated workers anywhere. Prior to the hurri- canes and storms, companies activated mutual assis- tance networks and prepositioned thousands of lineworkers and support personnel into the affected areas, so they could hit the ground running as soon as it was safe. This provided badly needed support for impacted companies, helping to restore power to communities safely and more quickly than in the past. We also are proud of the pivotal role EEI played last year in organizing and supporting the industry’s response in Puerto Rico following Hurricane Maria. The 3,000 men and women who came together from across the industry to restore power to the people of Puerto Rico truly represented our industry at its finest. We will never forget the incredible spirit of the Puerto Rican people, and we know that many of the men and women who worked on the island say the experience has changed them forever. Last year also marked one of the first times an EEI member company has used mutual assistance in response to a wildfire. The unprecedented devastation caused by wild- fires across the West highlights the continued need for our industry to look collectively for strategies to manage and mitigate the wildfire risk. To that end, EEI has established a wildfire practice, and we are:

Adding a high-tech element to our industry’s culture of mutual assistance, EEI has worked through the ESCC to establish an industry-wide cyber mutual assistance program, which now includes more than 150 electric and natural gas companies. Collectively, we are focused on developing a strong culture of security across the energy sector. As critical infrastructure providers, we understand we are a high-value target for adversaries. This is why we continue to improve our defenses, but also have focused on response and recovery—just as we do with storms—to ensure any impacts to our systems are limited and that we can help protect our nation’s security and the safety of our customers. It is important to recognize that during this time when division and disagreement often take center stage, all segments of the energy sector have found common cause to work together on the critical issues of secu- rity and storm response. This unity across the busi- ness models, with our natural gas counterparts, and with government leadership has provided extraordi- nary benefit to our customers and our communities. Tax Reform Implementation Last year at this time, EEI and our member compa- nies were celebrating congressional passage of pro-growth tax reform legislation, which was a major industry accomplishment that benefits our customers and our companies. To date, EEI member companies have announced almost $7 billion in tax reform benefits directed back to customers. Throughout last year, EEI worked with the Depart- ment of Treasury and the IRS, calling for the correct technical implementation of the industry’s priorities, particularly the appropriate allocation of interest on holding company debt. Regulations proposed in late November favorably address many of our issues. Most important, Treasury adopted the posi- tion that the industry exception to the interest limita- tion would be applied to the consolidated group and strongly supported EEI’s position regarding alloca- tion of interest on the basis that funds are fungible within a group. This year, we will continue to advocate for any neces- sary technical fixes and for the correct regulatory implementation to ensure the appropriate treatment of interest for holding company debt. ESG/Sustainability More than ever, we know that investors are looking for accountability from electric companies regarding their practices concerning the environment, social responsibility, and corporate governance, and the industry is responding. Last year, EEI launched a first-of-its-kind, industry- wide ESG/sustainability reporting template that was developed specifically for investors, with direct input from our industry’s major institutional investors. The template helps member companies provide inves- tors, Wall Street analysts, and other key stakeholders with more consistent and uniform ESG/sustainability data and information delivered in a timely way. As ESG-related issues further influence shareholder actions, this comprehensive reporting tool supports transparency and helps member companies receive credit for the incredible work they are doing. We expanded the template in November to include members of the American Gas Association (AGA), and we will continue to refine and advance the template going forward. We also are very proud of what our industry is doing to ensure that companies reflect the wonderful diversity of the communities that we serve. Today, a diverse and inclusive workplace is a social and busi- ness imperative. Last year, EEI developed a Diversity & Inclusion (D&I) Commitment that was endorsed by our Board of Directors in June. Not only is D&I taking hold in the industry’s general workforce, but in C-suites and board rooms as well. Regulated electric companies have more than three times the percentage of women CEOs compared to S&P 500 companies. Natural Gas Sustainability Initiative As noted earlier, as electric companies continue to transition their generation mix to cleaner resources, the share of electricity generated from lower- emitting natural gas continues to increase. In fact, the electric sector is now the largest customer for natural gas. Building off the success of the ESG template, EEI now is working with AGA and midstream and upstream natural gas associations on a new initiative focused on natural gas sustainability. The Natural Gas Sustainability Initiative’s (NGSI’s) priority is to demonstrate that the entire natural gas supply chain is becoming more sustainable from an ESG perspec- tive. The goal is to show our investors, customers, regulators, and other key stakeholders that we are committed to using natural gas that is sourced from environmentally sound and sustainable processes. A working draft of the NGSI conceptual framework encompasses the entire supply chain and focuses on the development of two key elements—consis- tent measurement of methane emissions along the natural gas supply chain and the transparent disclo- sure of these emissions. In addition, reporting will include acknowledgment of those companies that are meeting or exceeding sustainability goals. Industry Financial Highlights A hot summer across much of the country powered electricity demand higher in 2018. Electric output grew by 4.2 percent in the third quarter and by 3.1 percent for the full year, reaching a record high that marginally surpassed 2007’s total output. The gain was largely due to weather, as weather-adjusted output was flat year-to-year. Data from the National Oceanic and Atmospheric Administration show nationwide cooling degree days were 14 percent higher in Q3 2018 than their 10-year average, and 17 percent higher versus the same quarter last year. Our industry remains the most capital-intensive industry in America. For the seventh consecutive year, we expect another industry record, with total capital expenditures projected at $127.1 billion in 2018. Industry capital expenditures, which have tripled since the cyclical low in 2004, continue to be an important growth engine. Member company projections indicate that invest- ment in the generation segment decreased in 2018 compared to recent years, but we expect to see an elevated level of investment in the transmission and distribution (T&D) segments. Distribution continually has increased on both an absolute and relative basis over the past five years, while transmission held a relatively constant share of total capital expendi- tures, but increased on an absolute basis. Together, the T&D segments comprise about half of our indus- try’s total capital expenditures. Natural gas-related spending continues to increase steadily as many of our companies have expanded natural gas operations, both organically and through acquisitions. The gas-related segment captures spending on pipeline and delivery infrastructure, not natural gas-based electric generation. The EEI Index gained 1.3 percent in Q4 and returned a positive 3.7 percent in 2018, outperforming the major averages by 10 to 12 percentage points in Q4 and about seven to eight percentage points for the year. The EEI Index has produced a positive total return in 14 of the last 16 years. The industry’s funda- mental outlook was little changed in 2018, with most companies pursuing investment programs focused on regulated operations and targeting earnings growth rates in the mid-single digits with similar dividend growth. Our industry extended its long-term trend of wide- spread dividend increases in 2018. A total of 39 companies increased their dividend last year, compared to 38 in 2017, 40 in 2016, 39 in 2015, 38 in 2014, and 36 in both 2013 and 2012. Companies that raised their dividend in 2018 represented 93 percent of the industry, a new record high that surpassed 2016’s 91 percent. The average dividend increase- per-company during 2018 was 6.1 percent, with a range of 1.2 percent to 18.8 percent and a median increase of 5.6 percent. The industry’s dividend payout ratio was 54.4 percent for the 12 months ended September 30, 2018, remaining among the highest of all U.S. business sectors. As of December 31, 2018, 41 of the 42 compa- nies in the EEI Index were paying a common stock divi- dend. Importantly, the Tax Cuts and Jobs Act, which was signed into law in December 2017, maintains pre- existing tax rates for dividends and capital gains. This is crucial to avoid a capital-raising disadvantage for the high-dividend companies in our industry. The industry continues to strengthen its credit quality, which is currently a BBB+ average (S&P scale). Prior to its latest notch increase in 2014, the industry average had remained unchanged at BBB since the early 2000s. In terms of total credit actions in 2018, downgrades slightly outnumbered upgrades. From 2013 through 2017, credit actions were predom- inantly positive in each year as electric companies continued to build upon their regulatory relation- ships and to focus on their regulated operations. This long-term improvement in credit is correlated with the gradual transition to a more regulated business model. It is widely known that electric companies have been pursuing a back-to-basics approach to their businesses since the early 2000s. In fact, between 2003 and 2017, the industry moved from a balance sheet that was 63 percent regulated to one that is 81 percent regulated. This is especially important as our capital investment levels have risen dramatically. Conclusion When visitors and EEI employees step off the eleva- tors and into EEI’s offices in Washington, they are greeted with a Thomas Edison quote: “What you are will show in what you do.” EEI’s member companies already are making signifi- cant strides in carbon reduction, deployment of renewables, transportation electrification, and more. Among large industrial sectors, we are far and away out ahead as we work to deliver—and to lead— America’s energy future. Now, more than ever, we are working to show the way forward by demonstrating how we can come together as an industry to resolve challenges and to serve our customers and our communities. In doing that, we achieve our best

0 Comments

How Socially Responsible Investing Lost Its Soul

https://www.bloomberg.com/news/articles/2018-12-18/exxon-great-marlboros-awesome-how-esg-investing-lost-its-way ESG funds that promise to align your money with your values are often more marketing than science. “It’s easy to invest in what you believe.” That’s the pitch for TD Ameritrade’s foray into socially responsible ETFs, one of the year’s hottest financial crazes. Whether it’s climate change or gender diversity, today’s activist age has spawned an array of funds designed to appeal to millennials with a cause. And everyone, from BlackRock Inc. to Goldman Sachs Group Inc. and hedge fund titan Paul Tudor Jones, is jumping on the bandwagon. Yet Wall Street’s embrace has come at a steep price. All too often, critics say, revenue-chasing triumphs over principles. Investors who think they’re buying environmental, social, and governance funds—ESG for short—to promote a better world often wind up with costlier products that are, in almost every other respect, the same as any index fund. Criteria are so broad and disparate that companies as unlikely as Exxon Mobil Corp. and Philip Morris International Inc., the maker of Marlboro cigarettes, make the cut in some cases. In other words, ESG lost its soul in the bargain. To the naysayers, what began as a way to make a difference has become little more than an avenue for Wall Street to reap big profits, all while gaslighting the American public. “There’s a lot of greenwashing,” says David Krysl. A 28-year-old data science analyst from San Diego, Krysl was one of those millennials motivated by the prospect of doing good when he went to invest about $10,000 of retirement savings. Fossil fuels, guns, and cigarettes were no-nos. He wanted to reward companies with women and people of color on their boards. Socially responsible investing used to be the granola of finance After poring through scores of different options—many of which he found wanting—Krysl used some of his money to buy a clutch of ESG funds from Nuveen, whose tag line reads: “Align your investments with your values.” But recently, he learned one ETF owns Coca-Cola Co.—which he says is sucking up water rights around the world. (Nuveen says Coke’s water-stress issues have been “less severe” than its peers, and the company scores highly on its carbon footprint and waste.) Krysl is considering moving his money again. “They’re just banking off most people not having the time to really look.” It’s not hard to see why. As fees tumble toward zero in the $3.5 trillion U.S. market for exchange-traded funds, asset managers are desperately trying to come up with new products to sell and more ways to generate revenue. Many have zeroed in on slicing and dicing the investment universe into ever more specific themes (see robotics ETFs), or styles such as momentum. Though many funds are backed more by marketing than science, they all have one thing in common: higher fees, which firms say are justified because they do something more sophisticated than tracking the stock market. Assets in ESG Funds Have Surged Since 2015 Cumulative growth in percentage terms, starting in 2013 And these days, the hot new thing is ESG, a story that Wall Street can sell. In the past three years, ETF assets have more than tripled in the U.S., to $7 billion. Almost three-quarters of the funds have started since 2015. And more than 6,000 separate ESG indexes were created in just the 12 months through June. “There’s been a rush to occupy this space with not much substance,” says Francesco Ambrogetti of the United Nations Capital Development Fund, which helped design an ETF that donates its fee to the organization. “They promise a lot but don’t have a serious, rigorous system in place.” Granted, ESG is still a tiny sliver of the fund universe. But the fees have money managers seeing dollar signs. Compared with the iShares Core S&P Total U.S. Stock Market ETF, which costs 0.03 percent, investors pay on average 15 times more for do-gooder ETFs. (Nuveen, which charges 0.2 percent to 0.45 percent, says its prices reflect a methodology that’s more akin to active management.) That means an ESG fund managing $100 million can easily outearn a vanilla ETF that has over $1 billion in assets. With millennials such as Krysl projected to inherit some $30 trillion in coming decades, it’s no wonder ESG has become such a big deal. BlackRock, for instance, will introduce sustainability scores for more than 700 iShares ETFs early next year. Rich Rewards On average, socially responsible funds like Nuveen's earn 15 times more than the cheapest stock ETFs for each dollar invested Fee revenue for every $10 million in assets under management In some ways, ESG has become a victim of its own popularity. Socially responsible investing used to be the granola of finance—a niche where profits were an afterthought. One firm donated its fee to Unicef; others shunned companies that made money off pollutants, weapons, and smoking. Cutting out entire industries invariably hurt performance. However, if Wall Street could convince the investing public that an ethical choice could also be a reasonably profitable one—that could be a big moneymaker. So as the buzz around ESG grew, firms reinvented the category as a catchall for any company trying to do better in its field. Take the $1.2 billion iShares MSCI KLD 400 Social ETF. It promises “exposure to socially responsible” companies and can be used to “invest based on your personal values.” Yet a quick look shows it owns half the S&P 500. A Vanguard ESG fund holds 4 out of every 5 stocks in that index. BlackRock declined to comment on the overlap between its ETF and the S&P 500, saying it’s ultimately about how investors want to achieve their financial and ESG goals. Vanguard Group says its fund can be used as a core holding by those interested in sustainable investing. Fund providers often focus on the “G” in ESG The largest holding in a $22 million OppenheimerFunds ETF is Exxon Mobil, which has been accused by regulators of misleading investors about the cost of climate-change regulation. The fund, which buys companies with “best in class” ESG practices and shuns those that score poorly on controversies, also owns Philip Morris and at least three defense contractors. Oppenheimer says the companies garner above-average ESG scores, based on third-party research that specializes in sustainability analysis. The irony is that, while ESG funds look and act more like your average ETF (about 10 beat the S&P 500 in the past year), many ordinary investors aren’t all that fussed about returns. Those who spoke with Bloomberg said they were skeptical about how ESG funds were labeled and complained about the lack of products aligned with their particular priorities, such as worker welfare. Performance wasn’t a primary reason in their decision-making. “Millennials are the ones that want to invest in companies where their dollars are not going toward killing the whales,” says Jay Gragnani, head of research and client engagement at Nasdaq Dorsey Wright, which runs an ESG managed account. “It’s probably pretty difficult for the average investor. There’s a lot of information out there and, in some respects, too much information.” That’s partly because there’s little agreement over what constitutes ESG. Fund managers use different rules made by different index compilers, all of which can lead to radically different assessments for the same company. Lower emissions or a good safety record may win over millennials worried about environmental or social issues. However, institutions might reward a company simply for good governance—even in an industry like oil production. Even proponents such as Matthew Bartolini, head of Americas research for State Street’s ETF business, say ESG isn’t an exact science. The firm’s low-carbon target ETF, for example, owns Royal Dutch Shell Plc. “Is it really the purest form of clean power? Probably not,” he says. “There’s no true-north definition of ESG. That’s why you’re seeing a lot of different products come out.” Indeed, fund providers often focus on the “G” in ESG because it can be easier to quantify and measure. On Main Street, though, they continue to market ESG as a way for Americans to align their money with their values. Some are trying to make that true. Impact Shares, which started its first ETF in July, works with the NAACP and the UN, and donates its fees to charity. Others are ditching ETFs altogether. Swell Investing, where Krysl has most of his money, offers separately managed accounts that allow investors to buy stocks around specific themes, like disease eradication, and exclude names they don’t like. “We’re pushing a model where people are consciously putting their money toward things they care about,” says Jake Raden, who co-heads Swell’s impact team. “I’d hope that over time, ESG products fit more holdings-wise with what they purport to be, or that they change how they market themselves.”  Two Business Cycles to Prepare for A Low-Carbon World

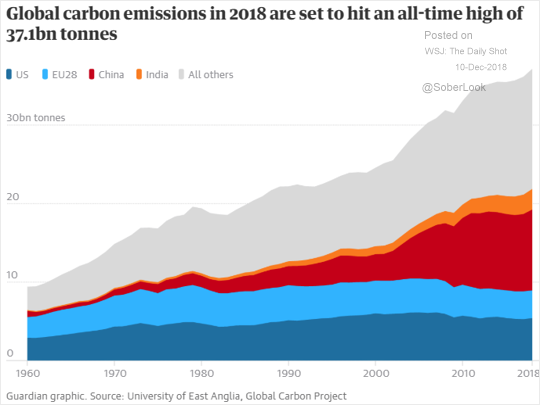

Refer:https://about.bnef.com/blog/liebreich-two-business-cycles-prepare-low-carbon-world/ December 7, 2018 Climate investment was $70 BN in 2016. 990 institutions with $7.2 TN of AUM declared some form of fossil fuel divestment. Going forward, 2,400 asset managers representing $82 TN have agreed to UN PRI commitment on ESG issues. Total AUM committed to PRI has grown 19% in the past 12 months. This week, as delegates from nearly 200 nations congregate in Katowice for COP24, the 24th annual UNFCCC conference on climate change, ‘tis the season to take stock of the state of climate politics around the world. Spoiler alert, it’s not a particularly jolly read. Paris, at least on the surface, serves as a great metaphor for global climate politics. Three years ago, those same COP delegates gathered with their political masters in the City of Lights to sign an historic agreement committing the world to limit global warming to below 2°C. Today, Paris is again in the news – but this time for riots triggered by increases in fuel tax designed to help deliver France’s climate goals. Lofty ideals, soaring rhetoric, ambitious targets – meet popular push-back! But is Paris really shorthand for what the state of the climate world, or is the reality more complicated? Reasons to be fearful Events around the globe certainly make it easy to paint a picture of climate policy in disarray. Exhibit A is, of course, President Donald Trump’s decision in June 2017 to pull out of the Paris agreement. But this year has delivered a number of other high-profile examples. Ontario Conservative Premier Doug Ford campaigned and won on a promise to pull the province out of its cap-and-trade scheme. Tony Abbott and his merry fossil-funded clique in the Australian Liberal Party used concern over the cost of climate action to wrest control from more moderate colleagues for the second time. A year ago, Scott Morrison was brandishing a lump of coal on the floor of the Australian parliament and telling his fellow MPs not to be scared of it; today he’s Prime Minister. In Brazil, during his successful presidential campaign, Jair Bolsonaro used a threat to quit the Paris Agreement to signal his business-friendliness. He has since relented, but one of his first acts as President was to rescind the country’s offer to host the next COP meeting after Katowice. China is once again using coal-fired power station construction as a means of delivering economic stimulus at home and securing influence overseas. Even Germany’s commitment to climate action looks wobbly. The ruling coalition’s governing document abandoned the country’s 2020 goal of a 40% emission reduction over 1990 levels, replacing it with a longer-term goal, and abrogated the selection of a year by which the country’s coal-fired power plants would be closed – delegating the decision to a special “Coal Commission” that looks set to miss its year-end reporting deadline. Global emissions, almost flat between 2013 and 2016, returned to growth in 2017, and will be up again in 2018. Once again, the European Union has proven long on rhetoric but short on action: with emissions growth of 1.5% in 2017, it has no moral high ground in Katowice from which to lecture the U.S. – where coal plants continue to close and emissions to drop. But before you conclude that the world is failing to address the climate challenge, and that wait-and-see or business-as-usual are viable business strategies, read on. Reasons to be cheerful, part 1: it’s not all about climate politics First of all, you should never assign excessive weight to global climate diplomacy. After all, what are the delegates gathering in Katowice to discuss? The Paris Rule-Book. I’m sure climate aficionados will in time treat the eventual product with the reverence of a Medieval palimpsest, but I can only get so excited about a set of binding rules designed to track voluntary commitments. The struggle to produce the Rule Book is in reality another skirmish in two ancient (in climate negotiation terms) conflicts between the developing and developed worlds. The first revolves around whether both should follow the same procedures to track commitments, with the developing world arguing for leniency and the developed world pushing back; the second is the old chestnut of climate finance, with the developing world trying to shake down the developed world for $100 billion annually by 2020, as promised in 2009 in Copenhagen, and even bigger sums beyond. It’s not quite two bald men arguing over a comb, but not far from it. The UN Framework Convention on Climate Change recently reported that north-south climate investment reached $70 billion in 2016; so just a 9% annual increase over the remaining four years would see the developed world live up to its Copenhagen commitment – not that this will mollify many developing countries, which wanted the money to be handed to them to spend as they saw fit, rather than invested in directly relevant projects. Meanwhile, the topic that should urgently be on the agenda in Katowice – trade – is missing. In 2016, the world’s major emitters failed at the last moment to sign an Environmental Goods Agreement that would have significantly lowered the cost of clean energy and transport; today, they are turning those same sectors, so vital for climate action, into battlegrounds in the trade war that is the biggest current threat to the global economy. This needs to stop. Perhaps the most interesting thing about the talks in Katowice is that U.S. negotiators – many of them the same people as have been negotiating for years – seem as interested as ever in winning negotiating points, despite the fact that officially the U.S. is pulling out and will not be bound by the results. It does rather look like they are hedging their bets, in case either the current unpredictable President or the next one recommits the country to the Paris Agreement. Reasons to be cheerful, part 2: clean energy and transport fundamentals Just as the Paris Agreement in 2015 did not drive the precipitous drop in wind and solar power prices that began in 2010, any agreement in Katowice is not needed to drive the mainstreaming of electric vehicles that began a few years ago. Climate economics precede climate diplomacy, not the other way around, and the economics keep looking better and better. In the second half of 2018 alone, the BNEF global benchmark levelized cost for solar fell by 14% and the wind benchmark by 6% (client links: web | terminal). Despite cutting support for solar power mid-year, China looks set to install another 40GW by year-end, down around 25% on last year, but with the entire shortfall set to be taken up by growth in other markets. 2018 might end up seeing the slowest rate of growth for PV installations globally since at least 2012, but the big Chinese solar manufacturers are all planning two- to three-fold increases in capacity in the next two to three years. The solar industry will return to strong growth in the near future, powered by its unbeatable value proposition, as well as strong national and sub-national policy signals – such as California’s pledge to reach zero net emissions by 2045, Spain’s target of 100% renewable power by 2050, and Queensland, Australia’s promise to reach net zero emissions by 2050. The wind industry is set to have its second-best year ever, with around 55GW added. The next few years will see installations get into record territory, with 30GW of new projects in the U.S. alone by 2020, and the arrival of giant offshore turbines which will power over 100GW of offshore projects by 2030. In transportation, 2018 saw demand for electric cars reach 5% of sales in China; China’s internal combustion car market is flat, with all growth now being absorbed by EVs. Progress has been a bit slower in Europe and the U.S., with sales only reaching around 2% of new cars but, with the launch of the Tesla Model 3 and hundreds of new models from big manufacturers reaching the showrooms, things are going to be moving fast. On the streets, the Charge of the Chargers has begun – and it’s going to be a battle royal between big oil and big utility. Shell has bought New Motion, BP has bought Chargemaster, Total has bought G2mobility. Equinor-backed Chargepoint has just closed a $240 million Series H funding round – with Chevron, among others, as an investor. (Disclaimer: I am a minor shareholder in Chargepoint.) Lithium-ion battery production reached an important milestone in 2018, with more than 50% of output devoted to EVs, rather than consumer goods. The battery supply chain may look a bit constrained between now and 2021, but at that point lithium-ion manufacturing capacity will soar to 630GWh, three times current output. Tesla’s 100MW, 130MWh Hornsdale Power Reserve battery has proven unbeatable at providing short-term grid services, earning its owners very healthy returns in the process. These pioneering sectors of wind, solar, EVs and batteries are being joined by others. The digitization of energy and transport infrastructure is starting to create value in the billions of dollars. Utility-of-the-future business models, designed around time-of-day pricing, are starting to get real traction. The next generation of clean technologies in heat, industrial processes, recycling, shipping, heavy road transportation and power-to-gas are readying themselves in the wings. Over 150 million people in the developing world have received their first ever modern energy services courtesy of distributed systems. It is clearly riskier to bet against this march of clean energy and transportation than to bet on it. Reasons to be cheerful, part 3: finance is waking up to climate risk and disclosure The third reason that investors and executives need to beware of misreading the Zeitgeist is that shareholders and lenders are becoming increasingly uncomfortable with high-carbon business models. While only 990 institutions – with $7.2 trillion under management, just 3% of total global savings – have actually declared some form of fossil fuel divestment, these are only the lead steers. More importantly, the main herd of investors is spooked and starting to eye its escape route. The UN Principles of Responsible Investment (PRI) commit asset owners and managers to incorporate environmental, social and governance issues, to seek disclosure from the entities in which they invest, and to disclose their own ESG activities. Climate and emissions are, of course, core areas of ESG focus. Nearly 2,400 major asset owners and asset managers with $82 trillion under management have already signed up to PRI, with total assets subject to PRI growing by 19% in the past 12 months. PRI is on its way to becoming a global industry standard. Another important initiative is the Task Force on Climate-Related Financial Disclosures (TCFD), set up in 2017 at the request of Mark Carney, Governor of the Bank of England and chair of the Financial Stability Board, and with Michael Bloomberg, founder and majority owner of Bloomberg LP as chairman. By September, institutions with over $100 trillion of assets under management had indicated support for its recommendations. It’s not just about disclosure and scrutiny. Activists are becoming more confident, more organized and more confrontational toward those delaying climate action. New climate warriors on the block, Extinction Rebellion, underlined their radical credentials last month by occupying the offices of Greenpeace, accusing them of being complicit with the corporate world’s dash through the planet’s remaining carbon budget. The Sunrise Movement – supported by new Democrat superstar Alexandria Ocasio-Cortez – occupied the office of U.S. Democrat party grandee Nancy Pelosi. Some 15,000 Australian school children took part in a one-day school strike to protest their government’s lack of climate action. Investors and executives should be concerned not just about direct action by activists, but about the threat of legal jeopardy into which excessive emissions or poor climate governance may place them. So far only Mexico and the U.K. among the major economies have enacted binding climate legislation, the London School of Economics has identified 25 climate-related lawsuits brought against governments or their representatives. The courts have already ruled against the Dutch government, forcing it to accelerate cuts in carbon emissions. In the U.S., a number of cities and counties in California, New York, Colorado, Washington and Maine have filed civil lawsuits against oil and gas companies. The landmark Juliana versus United States case pits 21 plaintiffs aged between 11 and 22 against the U.S. Federal government. Even if it is thrown out, the NGO coordinating it, Our Children’s Trust, has initiated similar suits in state courts from Alaska to Florida. The era of corporates and investors turning a blind eye to climate change, pretending it presents no risk or treating it like someone else’s problem, is surely drawing to a close. Reasons to be cheerful, part 4: When in the pits, look out for the pendulum The fourth reason why investors and executives should not take their cue from the words of anti-climate populists is that those populists may shortly find themselves on the losing side of history. In the 2018 midterm elections, President Trump hung onto enough seats to maintain Republican control of the Senate; Democrats gained control of the House and picked up seven governorships. Three of them – Nevada, Maine and New Mexico – were in states where renewable energy mandates had recently been vetoed by Republican governors. Wisconsin’s governor-elect, Tony Evers, campaigned on a pledge to join 17 other governors committed to the goals of the Paris agreement. Clearly the public likes renewable energy a lot more than many corporate leaders or lawmakers think. Climate action at the sub-national level is in robust good health. In the run-up to Katowice, the Climate Group, Carbon Disclosure Project and PwC reported that 120 states and regions from 32 countries, representing 21% of the global economy and 672 million people, have signed up to their own climate targets. Most pledges were from members of the Under2 Coalition, committing to reductions of 6.2% per year, the rate required to keep the planet below 2°C of global warming. In Australia, Morrison’s time as Prime Minister looks set to be limited. In October, he lost his parliamentary majority when outsider Kerryn Phelps, campaigning on a platform including support for climate action and opposition to the controversial Adani Carmichael coal super-mine, won the by-election in Malcolm Turnbull’s old seat. The country must hold a general election before May next year, and electoral meltdown for the Liberals is a distinct possibility. Canada is an important market to watch in 2019. Ottawa has decreed that all provinces must impose a carbon price of at least C$20. Those states that do not already do so will be subject to a Federal levy, but it will be returned directly to residents. The experiences of Australia and Ontario have showed how easy it is for populist conservatives to attack carbon taxes or credit auctions that are not fiscally neutral. If Canada’s scheme secures good public support, that will surely encourage fans of Carbon Fee and Dividend, the fiscally neutral approach promoted in the U.S. by the bipartisan Citizen’s Climate Lobby. Even when it comes to the riots in Paris, the lesson is not that the public reject any and all action on climate. It is that the public expects climate action to be efficient as well as effective; policy to focus as much on the carrot of affordable clean solutions as on the stick of raising the cost of dirty ones; costs to be equitably shared; and for the benefits to be clearly communicated. Make no mistake, the political pendulum is on the move back toward rapid climate action almost everywhere in the world. Some thoughts on business cycles and speed of change If the past 15 years have demonstrated anything, it is that the transition to clean energy and transportation will not be smooth. It will continue to be characterized by cycles, every six or seven years. The first cycle of the modern clean energy transition ran from 2004 to 2010. We saw an explosion of interest in clean energy; investment grew from around $100 billion per year to $350 billion; cleantech went through its big bubble; many were foolishly optimistic and ended the cycle bitterly disappointed. The second cycle has run from 2011 until now, producing dramatic falls in wind and solar costs, and the beginnings of real scale. While investment stalled at an average of $350 billion per year – around one dollar in every six invested in the energy sector – by the end of 2018 wind and solar were generating around 7.5% of all electricity in the world. The idea of the six- or seven-year business cycle is useful in thinking about how the energy and transport transition might play out. Bill Gates’s favorite economist, Vaclav Smil, points out that it took the better part of a century for coal to displace wood, or for oil and gas to start displacing coal; however, Peter Tertzakian, executive director of ARC Financial Corporation, urges us to focus on transformations market by market. What we see is that in one business cycle, sectors can be utterly transformed. In the past six years, LED lighting has gone from less than 5% of the global lighting market to more than 40%; coal in the U.K. has gone from over 40% to under 5%; plug-in vehicles in Norway have gone from around 5% of sales to nearly 50%. The recent Intergovernmental Panel on Climate Change Special Report (SR15), published this October, makes clear that by 2030, one of two things will have happened: either we will have reduced emissions by 45%, or we will have burned through the remaining 580 GtCO2 carbon budget for a 50% chance of holding average temperature increases below 1.5°C. For a 50% chance of keeping below 2°C, the required emission reduction by 2030 still has to be at least 20%. That is just 12 years away. Think about it: not only does each 6-year business cycle bear the risk of destroying businesses or business models that currently look impregnable; in just two business cycles – well within the range of our remaining careers – we will find ourselves in a world where either carbon emissions are dramatically lower, or there will be no remaining carbon budget, and presumably no societal license to operate carbon-intensive businesses. Once you accept that the world is going to look very different at the end of the next two business cycles, whether we listen to the warnings of scientists or not, priorities become refreshingly clear. Ignore the noise, focus on the signal. Trump is noise. Katowice is noise. Weather is noise. News is noise. The signal is, where do you want to be at the end of those two cycles? What portfolio do you want to own? What business do you want to be in? What business do you not want to be in? And – crucially – what do you need to do right now in order to get an edge on your competitors? I warned you I was not offering jolly seasonal thoughts. But hopefully they are thoughts you can turn into action. Perhaps more New Year’s Resolution than Christmas Cheer. Two business cycles. Don’t waste them.  Trends in Sustainable Investment: Energy Security, Environmental Sustainability and Affordability and Access.

Refer: https://www.greenbiz.com/article/can-energy-become-secure-affordable-and-sustainable-sector-transforms By 2050, up to 90% of OECD generation will be from renewables. IEA predicts renewables will be 40% global power generation by 2040. 400 global companies, cities, states and regions set 100% renewable energy targets Energy is at the root of modern economies and is vital to the Fourth Industrial Revolution and the internet of things. The challenge for policymakers is to craft policy frameworks that enable the three critical goals of energy security, environmental sustainability and affordability and access while the energy sector undergoes a fundamental transition. Maintaining a balance between these three goals creates a "trilemma," which is getting more complex for countries and energy companies — especially given the uncertain pace of the transition to decentralized, decarbonized and digital systems. Put differently, we are trying to build a bridge while crossing it. The comparative rankings and profiles of the 125 economies covered in the World Energy Trilemma Index 2018 highlight how the exponential acceleration of interconnected megatrends shaping the global energy sector are rapidly evolving the means to achieve and balance energy trilemma goals. Energy security Evolving energy sources are shifting the definition of and means by which to achieve energy security. In a fossil fuel-driven world, energy security was ensured by the security of energy supply. But technology has led to an increased supply of natural gas and has driven improved performance and reduced costs of renewables. Today’s energy security increasingly implies flexibility of a diversified grid, which is hard to measure and even harder to ensure. For example, coal-fired electricity generation in OECD countries is in terminal decline. Initially displaced by cleaner natural gas, it has been increasingly losing ground to renewable sources that continue to grow faster than predicted: The share of renewable generation has doubled every 5.5 years. Under these trends, coal-fired power and nuclear no longer will be viable sources of power in OECD countries by 2050. For example, in the United States, the share of electricity generated from coal dropped from 52.8 percent in 1997 to 45 percent in 2009, and then to 30.1 percent in 2017. Meanwhile, the share of natural gas in 2017 stood at 31.7 percent, and the share of renewables was at 17.1 percent. Today’s energy security increasingly implies flexibility of a diversified grid, which is hard to measure and even harder to ensure. On this trajectory, by 2050, up to 90 percent of OECD generation will be from renewables. The IEA predicts that the share of all renewables in total global power generation will be 40 percent by 2040 [PDF]. Looking outside the OECD, coal as a percentage of total electricity generation is expected to remain high in the near term. For example, coal is on track to grow to 75 percent in India by 2027 and to 56 percent in Indonesia in the near term. However, China may be indicative of future trends in other countries that hope to balance energy security, increased energy access and environmental sustainability. Coal is on track to drop to 56 percent of total energy generation in China — from 80 percent in 2007, as China continues its focus on increasing renewables. Fossil fuels are also affected by the movement to divest from fossil fuel [PDF], which has grown 11,900 percent from $52 billion assets under management four years ago to over $6 trillion today, with nearly 1,000 institutional investors pledging to divest from coal, oil and gas. This trend is likely to have increasing impacts beyond OECD countries in upcoming years. Along with this, investment in clean energy has grown at 14 percent CAGR over the past 10 years. Access and affordability Decentralization and democratization of the energy system will shift the definition of energy access and affordability. The adoption of renewable generation, distributed energy resources (DER), deployment of smart grids, energy storage solutions and electrification of transport are just some trends transforming the generation, transmission and distribution of electricity. Supplies of ever-cheaper mainstream wind and solar power are driving down wholesale electricity prices. The expansion of renewables is expected to further drive growth in battery storage capacity and subsequently decrease installation costs, further disrupting the traditional model of centralized power generation and distribution. Many incumbent utilities companies in Western countries are struggling to adapt, as their business models are perceived as in decline. They soon may be replaced by potentially new business models from challenger companies. Decentralization and democratization of the energy system will shift the definition of energy access and affordability. Under these forces, Europe will see a mostly decentralized and highly democratized energy system by 2040. Elsewhere, DER is creating new opportunities for low-income economies to provide secure, reliable and affordable energy through mini- or microgrids. The number of residential and industrial "prosumers" — those who both consume and produce electricity — at a local level is already rising. They soon will play a far more active role in the energy system as a whole as they look to manage energy costs and the sources of their energy, enabled by evolving technologies such as blockchain. For example, in September, Apple, Akamai, Etsy and Swiss Re leveraged their collective buying power jointly to purchase renewable energy in the U.S. PJM energy market with the largest aggregated corporate renewable energy transaction to date. Environmental sustainability Shifts in electricity generation and transportation fuels will help meet energy sustainability goals, and the energy transition will change the economics of the oil and gas industry. For example, recently, nearly 400 global companies, cities, states and regions set 100 percent renewable energy targets and/or zero-emissions targets, including California, the world’s fifth-largest economy, and companies with collective annual revenues of more than $2.75 trillion. Energy companies and regulators will have to adapt and develop innovative mechanisms to respond to these goals. The shift to electrification of mobility will affect liquid-fuels demand and create new competitors and collaborators. Consider the e-vehicle charging infrastructure initiative in California backed by the state’s three investor-owned utilities. The lines are blurring between utilities, O&G majors and investors as drivers of disruption challenge existing structures. As with other areas of the energy transition, the pace of electrification is uncertain but can be expected to grow rapidly. Regulations, including pressure to phase out internal combustion engine vehicles, are pushing the switch toward EVs, with predictions of worldwide e-vehicle growth at 11 million in 2025 and with China accounting for almost 50 percent of the global EV market. Countries and companies are battling for competitive positions in the changing mobility sector. The United Kingdom, for example, recently set out a plan to become the world leader in electric and zero-emission vans, trucks and cars. Looking ahead Leveraging evolving technology opportunities to simultaneously focus on the three aspects of the energy trilemma — security, equity and environmental sustainability — not only can grow economies, but also can transform societies. Yet the complexity of issues facing the globalized energy industry make them impossible for countries to tackle in isolation. Navigating through evolving policy and regulatory frameworks across states, along with innovating in the field of power generation, is key to achieving progress and maintaining balance. In this changing context, policymakers at all levels and those in the energy sector, both legacy and new players, must engage to ensure policy and regulatory frameworks enable economies and societies to fully leverage the new opportunities to meet the energy trilemma. How a Big Bank Fueled the Green Energy Boom

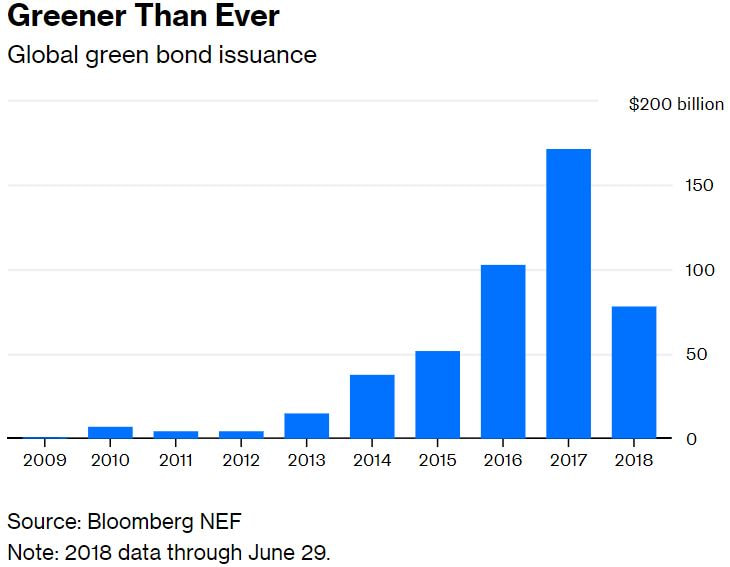

Source: Bank of America Wind and solar energy projects were struggling to attract investors. Then Bank of America got creative. By MATTHEW HEIMER OKLAHOMA IS AN EPICENTER of fossil-fuel production, a state where oil-well pump jacks punctuate the pastures. But if you drive out to Grady County, an hour west of Oklahoma City, you’ll encounter a different mechanical landscape. There, atop the hills outside Minco, dozens of 80-meter-tall turbines churn, their blades generating a steady drone to accompany the occasional dairy-cow bleat and the buzz of distant cars. This metallic display is part of Pioneer Plains, a sprawling wind-power project that generates electricity for some 42,000 homes. The turbines are part of a highstakes transformation in the energy economy—a bet that renewable power can scale up as a cost-effective replacement for fuels that contribute to climate change. But the wind farm is also a symbol of financial transformation: It might never have sprouted if it weren’t for “green bonds”—an investment vehicle that didn’t exist a decade ago. Those bonds were the brainchild of dealmakers at Bank of America—the $87 billion, 209,000-employee giant that occupies the No. 3 spot on Fortune’s Change the World list this year. Their work is part of BofA’s $125 billion Environmental Business Initiative, a campaign that has established the Charlotte based bank as a powerhouse in “climate finance”—the unglamorous but essential business of steering investor capital into the low-carbon economy. Green bonds, which the bank all but invented, have raised $442 billion worldwide since 2013, helping borrowers both tiny (the Antioch, Calif., Unified School District) and enormous (trillion-dollar Apple) pay for renewable-energy innovations. Courtesy of NextEraMost environmental advocates agree that a renewable revolution can’t happen without a big private-sector push. And a behemoth like Bank of America—with its web of relationships and deep pool of expertise—can make a decisive impact in connecting investors with cash-hungry green projects. “Doing the first-ever commercial green bonds, appealing to institutional investors—BofA gave this market credibility,” says Sean Kidney, cofounder and CEO of the Climate Bonds Initiative (CBI), a London nonprofit that tracks green-energy investing. “They’ve been invaluable.” IN AN ERA WHEN AMERICANS can buy solar power through their local utilities and run errands in Teslas, it’s hard to imagine that wind farms or solar-panel arrays ever went begging for funds. But a decade ago, during the financial-crisis catastrophe, that’s exactly what was happening. “Risk appetite was really diminished,” explains Suzanne Buchta, managing director of ESG debt-capital markets at BofA Merrill Lynch. “And most environmental investing was seen as risky.” At the time, Bank of America was paying a heavy price for misjudging risk. Bad bets on subprime mortgages had demolished its balance sheet. Fleeing investors wiped out more than 80% of its market value, and the bank wound up taking $45 billion in federal bailout money. Brian Moynihan, who was tapped as CEO in December 2009, found himself holding multiple rounds of soul-searching with his C-suite team. The bailout had been repaid by then, but the new theme, as Moynihan recalls it, was “Why are we here? Who would miss us if we were gone?” Bank of America’s leaders rethought their mission, retrenching around more conservative investing and basic business and consumer lending. During that pivot, Anne Finucane, then the bank’s global chief strategy and marketing officer, became convinced that green investing could fit under that umbrella. The bank had made a $20 billion commitment to such projects in 2007, and modest successes with projects like energy-efficient buildings had encouraged her and her team. “We were convinced by the business that we were doing that this could work on a larger scale,” Finucane recalls, “but we had to prove it.” In 2013 she got her chance: At her urging, Bank of America committed to deploying another $125 billion for “low-carbon and sustainable business.” That mobilized an army of employees to dream up and pitch new projects. Underwriters who could sell ideas to investors; energy-market traders who knew where clean power was in demand; engineers who knew the ins and outs of turbines and solar panels—BofA had plenty of employees in each category. Finucane, who’s now the bank’s vice chairwoman, acted as connector and advocate, bringing people from disparate teams together and helping them get buy-in from the top. “If you ask people to think outside their comfort zone, to work and think horizontally, a lot can happen,” she says. “We were taking people off the things that they knew how to do, and putting them on things they didn’t know how to do,” agrees Alex Liftman, Bank of America’s global environmental executive. “And they came up with ideas twice as fast as we expected. A decade ago, “Most environmental investing was seen as risky.” —SUZANNE BUCHTA, BOFA MERRILL LYNCH Courtesy of Bank of AmericaONE SUCH BRAINSTORMER was Buchta, the debt specialist. An avid hiker and nature lover, she had been mulling how to draw investors into green projects, and she knew bonds had advantages over stocks. One was stability: Bond interest is predictable, and only during major meltdowns do most bonds become as volatile as stocks. That makes bonds hugely appealing to the risk-averse pension-fund managers, insurers, and other institutional investors that oversee the lion’s share of global capital. Another advantage was “ring fencing”: Unlike stocks, bonds could be structured to require issuers to use the proceeds only for specific purposes. Beginning in 2013, Buchta collaborated with her counterparts at several big banks, hashing out some broad “Green Bond Principles.” A bond, they agreed, could be called “green” only if its proceeds paid for projects with a clearly positive environmental impact. Issuers would have to be transparent with investors about where the money went and how the projects progressed, and, ideally, an independent party would certify the bond’s greenness. “The brilliant thing about the concept is that it’s so simple and so easily accessible,” says Buchta: A green bond would offer investors a clear, verifiable connection between their financial commitment and a project that helps the climate. To test the concept, Bank of America played guinea pig. In 2013 it issued the first-ever “benchmark-size” (that is, big) corporate green bond. BofA borrowed $500 million from investors, deploying the proceeds into a dozen different projects. The funds paid for turbines at Pioneer Plains; they also helped upgrade some 170,000 streetlights in Los Angeles and Oakland with energy-saving LED bulbs, and enabled Antioch to build solar arrays at 24 schools. BEFORE AND AFTER: A view of Los Angeles from the slopes of Mount Wilson, before (bottom) and after (top) the city retrofitted tens of thousands of streetlights with LED bulbs, in a project financed in part by a Bank of America green bond. The orange glow is a sign of the energy “leaked” by traditional sodium bulbs. Courtesy of Los Angeles Bureau of Street LightingOn their own, those small, potentially risky projects would have struggled to attract lenders and would have borrowed at high rates if they could borrow at all. By bundling them and backing them with its own credit rating, Bank of America brought the cost down. (The three-year bond paid 1.35%—attractive to investors in a low-rate climate, but a bargain for borrowers.) And although the payout wasn’t huge, the bond issue was oversubscribed: With institutional investors seeking more green opportunities, there was more demand than there were bonds to sell. The market had its proof of concept—and other borrowers rushed in. The Commonwealth of Massachusetts issued the first municipal bond to be labeled “green,” in 2013. The giant utility Southern Co. raised more than $1 billion for solar and wind projects. Apple issued $2.5 billion in green bonds in 2016 and 2017, financing an effort to run more of its facilities on renewable power. BofA was the lead underwriter on each of those deals, playing matchmaker to attract investors. To date, it has underwritten $27 billion worth of green bonds, more than any U.S. bank. At the same time, a broader market has taken off. Since Jan. 1, 2017, there have been $254 billion in green-bond issuances, according to CBI—more than in the previous four years combined. Bank staffers take pride in the creative ways they’ve deployed capital for green causes. At Pioneer Plains (which is owned by NextEra Energy, No. 21 on the Change the World list) and two dozen other energy projects, BofA has used bond proceeds to make “tax equity” investments, paying developers upfront in return for the right to claim their green-energy tax credits. The deals give the developers funding for construction and repairs; the bank uses the credits to cut its own tax bill. Another BofA project, the Catalytic Finance Initiative, specializes in crafty climate-finance puzzle solving. Last year the CFI team helped Vivint Solar package the cash flows from 30,000 of its residential solar accounts into a $203 million bond and sell the debt to investors. A bond deal structured by Bank of America helped Vivint Solar raise more than $200 million. Courtesy of Vivint Solar BofA doesn’t break out how much revenue its environmental business has generated, but underwriting fees, loan interest, and advisory fees have made the enterprise profitable. To date, the bank has deployed more than $96 billion of the $145 billion it has committed to green business since 2007. Its own fortunes have improved lately too. Over the past three years, its stock has risen twice as fast as the S&P 500, and profits are up 20%. A bond deal structured by Bank of America helped Vivint Solar raise more than $200 million.In April, four economists released a working paper that gave green-bond fans reason for optimism. They found that municipal bonds labeled “green” paid six basis points (0.06%) less in yield than nongreen bonds—and that the effect doubled or tripled for bonds that took the extra step of being certified green. Bond yields fall when buyers drive up prices, so the lower yields suggest that demand for green bonds is stronger than the norm. On a typical muni bond, that could result in millions of dollars in savings on interest. Compared with those benefits, “the cost of certifying a green bond is modest,” says coauthor Jeffrey Wurgler, a professor of finance at the NYU Stern School of Business, while borrower and investor alike “get a green glow.” The urgent question is how much bigger and brighter that glow can get, and how quickly. Electric-vehicle production, energy storage, the building of “smart grids”—all are areas where great strides could be made, but only if the private sector can mobilize the money to fund them, at the rate of trillions per year rather than billions. “Public capital is not enough,” notes BofA’s Moynihan. “But private capital has to be accessed in a way that it’s used to being accessed.” If green bonds, with their relative stability and familiarity, lure more big money into the game, Bank of America will have done a lot to pave the way for it. Private Equity Firm TPG Plans to Raise Second Social Impact Fund